Recent EIA data and academic research show that ethanol consumption remains robust and on track to outpace last year’s numbers, even despite small refiner exemptions (SREs) and falling RIN prices. So much for the long-held claims of ethanol demand destruction … we hope … but surely there must be a bogeyman out there somewhere, right?

In fact, a new one has emerged just in time. The ethanol demand destruction myth is now facing competition from a fresh face: The claim that SREs and falling RINs are causing demand destruction to biodiesel. Brace yourself for another round of house-on-fire hysteria.

Yet a close examination of both the facts and history of the biodiesel mandate warns us against crying wolf once again. The stubborn fact remains that domestic biodiesel production is up compared to last year. And if in fact the product is in some way falling short of its potential, the more fair-minded out there would note that U.S. trade policy and a lack of clarity over the federal biodiesel tax credit would be lead factors in creating market uncertainty.

What’s going on, then? The massive tariffs levied against our nation’s biggest biodiesel import suppliers – Argentina and Indonesia – have boosted the fortunes of domestic biodiesel producers at the expense of these foreign suppliers. Ironically enough, they’re making it all the harder to meet RFS mandate levels. Perennial uncertainty around retroactive extension of tax incentives has also hindered biodiesel consumption growth.

History of the Biodiesel Mandate

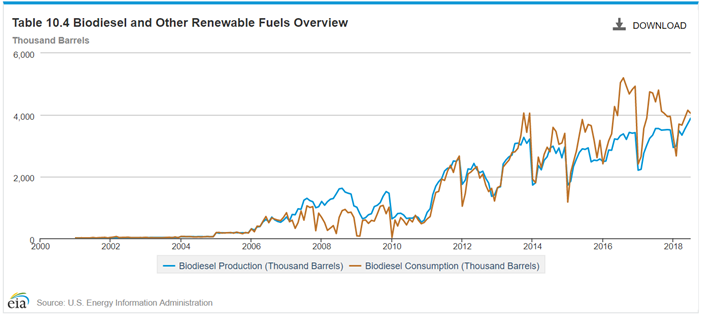

Over the last few years of the program, actual domestic biodiesel production has never been enough to meet the actual biodiesel mandate. Why? Biodiesel is a lot more expensive than petroleum diesel and needs significant artificial support to be economical. Additionally, domestic biodiesel producers have historically been less economically competitive compared to foreign suppliers. As a result, for the past several years, the RFS has essentially become a foreign biodiesel import mandate.

This reality is in part why the biodiesel industry advocated for massive tariffs on the primary foreign supplier of biodiesel to the U.S.; tariffs that the administration ended up instituting. Yet, as often happens with tariff protection, domestic producers prove unable to make up the gap. The result has been increased domestic biodiesel production (discussed below) matched with a continued inability for that domestic production to meet lofty domestic targets, resulting in a decline in the consumption of biodiesel relative to last year.

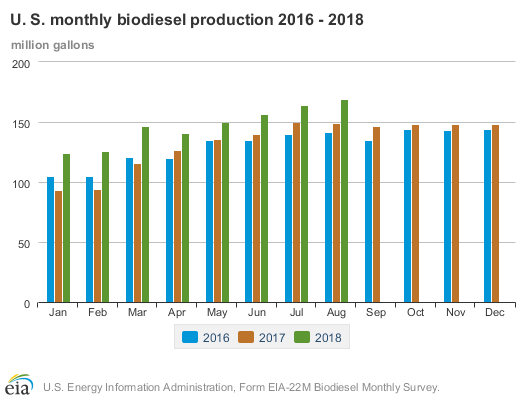

Domestic Biodiesel Production on the Rise

As tariff proponents had hoped, domestic biodiesel production has risen every single month this year compared to last year. In total, through the first 10 months of the year, domestic biodiesel producers have made over 242 million more gallons (generating over 362 million more RINs) than they did over the same period last year, according to EPA data. Production is the most relevant metric for biodiesel in relation to the RFS, because unlike conventional ethanol, biodiesel producers can separate and sell RINs attached to their fuel, instead of having to separate RINs at the point of blending (as with ethanol RINs).